Bookkeepers, accountants, and small business owners use trial balances to check their accounting for errors. The unadjusted trial balance is the initial report you use to check for errors, and the adjusted trial balance includes adjustments for errors. A trial balance is an accounting report you put together at the end of an accounting period to ensure the general accounting ledger is correct and the total debits match the total credits.

How Liam Passed His CPA Exams by Tweaking His Study Process

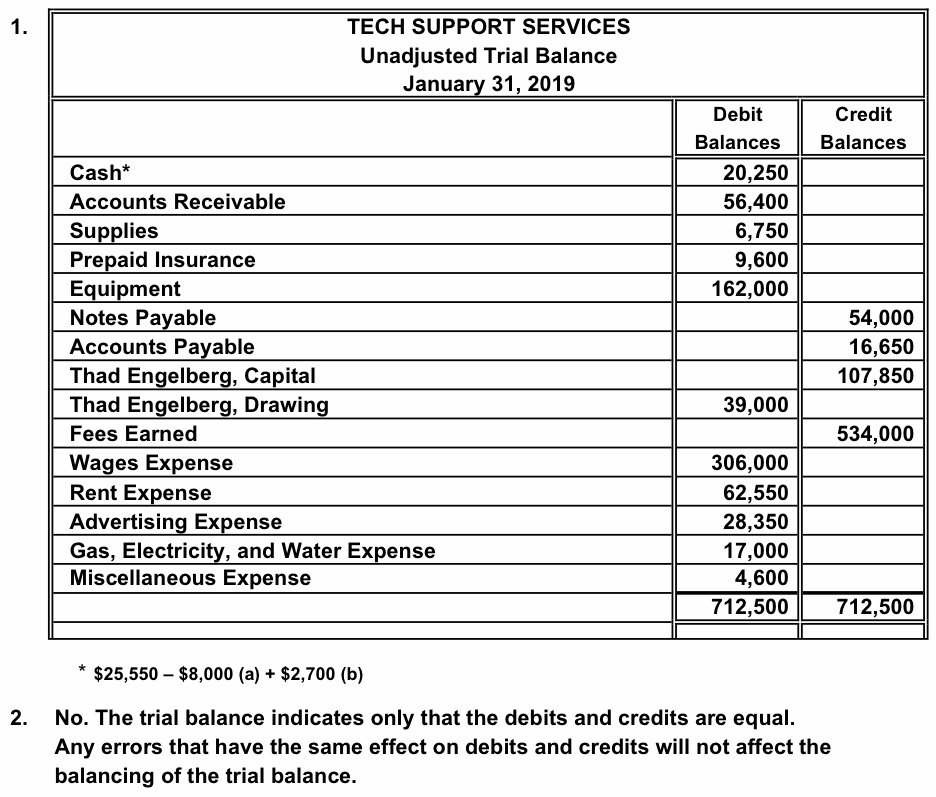

If numbers don’t match, you’ll know there’s an error somewhere that needs fixing. It acts as an initial diagnostic tool that signals whether further investigation is needed before proceeding with adjusting entries and eventual financial statement preparation. However, if totals are equal, it still does not fully guarantee that no errors were made; for example, when a transaction was recorded twice or when it was not recorded at all. It shows a list of all accounts and their balances, either under the debit column or credit column. Remember that transactions are recorded in the journal and posted to accounts in the general ledger. Figure 1 shows the unadjusted trial balance for Bold City Consulting, Inc., at March 31, 2018, after its third month of operations.

When is the unadjusted trial balance prepared?

The final total in the debit column must be the same dollar amount that is determined in the final credit column. For example, if you determine that the final debit balance is $24,000 then the final credit balance in the trial balance must also be $24,000. If the two balances are not equal, there is a mistake in at least one of the columns. There are eight steps in the accounting cycle, the fourth step being the preparation of an unadjusted trial balance. Companies have to have an organized and adjusted trial balance before they prepare their financial statements to reflect the liabilities, assets, revenues, and expenses of the organization. This means there might be an error in the ledger accounts or in the postings from the journal entries to the ledger.

- Note that while a trial balance is helpful in the double-entry system as an initial check of account balances, it won’t catch every accounting error.

- It lays out raw financial data straight from the accounting records, serving as evidence of all monetary transactions up until that moment.

- Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

- Preparing an unadjusted trial balance is the fourth step in the accounting cycle.

- Figure 1 shows the unadjusted trial balance for Bold City Consulting, Inc., at March 31, 2018, after its third month of operations.

How to prepare an unadjusted trial balance

Whereas, the adjusted trial balance (ATB) is the same as UTB except that it also includes any adjusting entries made during an accounting period. Managers and accountants can use this trial balance to easily assess accounts that must be adjusted or changed before the financial statements are prepared. There’s also a chance it’ll fail to flag entries incorrectly coded to the wrong accounts, which can ultimately lead to inaccurate financial statements. A trial balance plays a major role in the accounting cycle, notably at the end of an accounting period before generating financial statements. It is important to note that the unadjusted trial balance is prepared in traditional bookkeeping.

Notice the middle column lists the balance of the accounts with a debit balance, while the right column has balances for credits. You gather all account balances and line them up side by side in a trial balance sheet. This step is critical in painting an accurate picture of financial health before you make any adjustments. If this is the case, the trial balance will show the variance between the debit and credit sides. And the accountant needs to back to confirm the problem, then make adjustments.

A trial balance is an important step in the accounting process, because it helps identify any computational errors throughout the first three steps in the cycle. While every company maintains a record of its account balances in its general ledger, financial statements can only be complete and accurate if all accounts are prepared accurately. Unadjusted and Adjusted Trial Balance is done to prepare final accounts which can then be used as a basis for recording adjusting entries to prepare the adjusted trial balance. The purpose of the trial balance is to test the equality between total debits and total credits after the posting process. This trial balance is called an unadjusted trial balance (since adjustments are not yet included). It serves to be the source of all financial statements that a company creates.

In summary, the unadjusted trial balance (UTB) lists all accounts in an organization at a given point or period of time. It will contain all assets, liabilities, and equity accounts so they can be used to prepare your company’s income statement and balance sheet. After the accounts are analyzed, the trial balance can be posted to the accounting worksheet and adjusting journal entries can be prepared.

² In accrual accounting, revenue and expenses are recorded when they are earned or incurred irrespective of whether the cash is exchanged or not. After the all the journal entries are posted to the ledger accounts, the unadjusted trial balance can be prepared. An unadjusted trial balance is a listing of all the business accounts that are going to appear on the financial statements before year-end adjusting journal entries are made. While an unadjusted trial balance may uncover mathematical errors, the following types help in eliminating accounting errors and ensuring accurate financial statements. An unadjusted trial balance is typically prepared at the end of an accounting period before adjusting entries are recorded. Unadjusted trial balance is the list of the general ledger accounts balance (balance sheet’s items and income statement’s items) for the specific accounting period before making any adjustment.

Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. For information purchases journal format calculation and example pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing.

Making sure these numbers are right is super important for the financial statement to be correct. Accountants of ABC Company have passed the journal entries in the journal and posts the entries in to their respective ledgers. He then took all the balances of each account in the Ledger and summarized them in an unadjusted trial balance which is as follows.

Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible.